Excerpted from Business Week, “A Standoff Over How to Rescue the Housing Market”, December 11, 2008

* * * * *

http://images.businessweek.com/ss/08/12/1211_numbers/2.htm

Without reducing foreclosures and ending the slide in home prices, it will be nearly impossible to stabilize banks and lessen the depth of the recession. And sharply rising unemployment has added new urgency: Last spring, Rod Dubitsky, Credit Suisse’s (CS) head of research for asset-backed securities, projected 6.5 million foreclosures. With unemployment set to top 8% in 2009, he says up to 10 million families may lose their homes.

What’s the best way to stabilize plunging home prices?

Treasury Secretary Hank Paulson and his staff are considering plans to push mortgage rates down to 4.5% in hopes of bringing buyers back into the moribund market.

Democrats—in Congress and on President-elect Barack Obama’s team—seem more set on pressing lenders to renegotiate troubled mortgages. That tack, championed by FDIC head Sheila Bair, is aimed at trimming foreclosures and ending fire sales.

Bair’s plan offers a guarantee to lenders that modify a mortgage so payments are trimmed to 31% of a homeowner’s gross income. If they cut interest rates or stretch out the life of a loan, Washington would cover part of the lender’s losses should a homeowner redefault. Bair says the plan would save 1.5 million homeowners at a cost of $24.4 billion. [Note; lenders would get subsidies only on loans that redefault.]

But conflicting investor interests make it legally tough to modify securitized loans. And new statistics suggest that more than half of loans modified early this year are already at least 30 days past due.

Treasury says it’s studying several options, including the plan to subsidize low rates. Proponents say that by bringing new buyers to the market, the move could help end the pricing slide. Problem is, low rates would do little for those now facing foreclosure or trapped in homes worth less than their mortgages.

Full article:

http://www.businessweek.com/magazine/content/08_51/b4113030318539.htm?chan=top+news_top+news+index+-+temp_news+%2B+analysis

* * * * *

Ken’s Take:

In rough numbers …

- 2/3’s of roughly 125 million households are owner-occupied

- 1/3 of owner-occupied households are owned free and clear of any mortgage

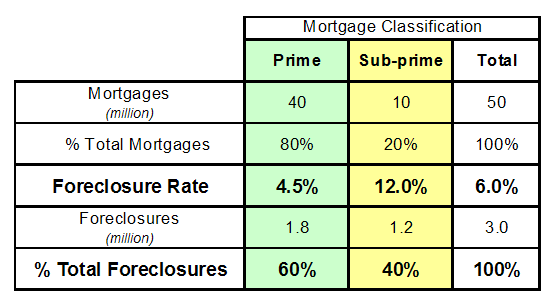

- 20% of mortgages are sub-prime; most with no down payment; many “under water”

- Vast majority of sub-primes were “unqualified” at fair market (vs. “teaser”) interest rates

- 12% of sub-primes are in foreclosure, accounting for 40% of total foreclosures

- 50% of foreclosed sub-primes don’t qualify at modified terms (e.g. writing loan down to house’s FMV)

- 50% of modified sub-prime loans re-default within 6 months

Bottom line: Many of the people being foreclosed on are “occupants” not “owners”. Help legitimate owners who are going through some tough times; stop delaying the inevitable for the sub-primes — and certainly don’t reward them with deals better than the people who played by rules have. That’s not fair !

* * * * *

Want more from the Homa Files?

Click link => The Homa Files Blog