If you’re up to speed on the proposals to modify mortgages to stop foreclosures, scroll down to Loan Modification Math …

Background:

There seems to be momentum to “keeping people in their homes” by modifying the bulk of the 4.6 million mortgages that are currently in foreclosure or payment delinquent for longer than 90 days.

There have already been some voluntary lender efforts to modify distressed mortgages by lowering interest rates or extending the term of the mortgages (say, from 30 to 40 years). Generally, the programs haven’t generated many modified loans … and for the loans that have been modified, about 40% become delinquent again within 6 months. (Note: I’ve seen ranges on this number from 35% to over 50%).

So, the Feds are pushing lenders to sweeten the mortgage modification packages. Specifically, there’s talk of a broadscale government program that would pare mortgage interest rates to 4.5%. And, there seems to be support for “cram downs” — having lenders reduce the principal loan balances to the current fair market value of the homes collateralizing the loans. That is, if a defaulting loan is on a home that is “below water” — i.e. loan balance is greater than the home’s market value — the lender writes off the difference and issues a revised mortgage at the home’s market value.

These proposals strike me as both naive and very problematic. In this and subsequent posts, I’ll summarize why I think cram downs are a bad idea.

* * * * *

Loan Modification Math

A frequent pundit refrain is that “you can’t get there with just rate and term adjustments — you have to reduce the loan balance to keep these loans out of foreclosure.” Not surprisingly, there’s a lot of hand-waving but few numbers.

For the record, here’s how the math works.

Say, a person buys a home for $150,000 with no downpayment (as is typical with sub-primes), a 10% mortgage interest rate (maybe a bit low for sub-prime loans), and a 30 year term. The monthly mortgage payment — for principal and interest — would be $1,269.

If the interest rate on the loan is cut to 4.5%, the monthly payment would drop by over 40% to $752.

If the interest rate is cut to 4.5% and the loan’s payback period is extended from 30 to 40 years, then the monthly payment would drop to $666. That’s about half of the original monthly payment! {Note: If the starting interest were more than 10%, the new payment would be more than half off).

Apparently, some politicos think that cutting the payment in half isn’t enough to make a difference. So, they propose that lenders accept “cram downs” and reduce loan balances.

Let’s assume that the home’s fair market value fell by 25% since the time of purchase. That would mean writing off $37,500 of the loan balance and reissuing it with a $112,500 balance.

If the interest rate is cut to 4.5%, the loan’s payback period is extended from 30 to 40 years, and the principal balance is reduced to $112,500, then the monthly payment drops to $499. That’s less than 40% of the original monthly mortgage payment — a discount of more than 60%.

Are these folks serious ???

Cutting the mortgage rate in half for a defaulter — while keeping the hardworking, creditworthy folks next door at the full rate — is morally bankrupt. Especially when the defaulter didn’t legitimately qualify for the loan by any reasonable underwriting standards … and is equally likely to default again.

What about the hardworking guy who has made payments for years but but just got got laid off in the tough economy? Well, the half-payment may even be too much for him to handle. Unfortunate, but true. I say the bank (and Feds) should give that guy plenty of breathing space (e.g. suspend payments for 6 months).

In a subsequent post, I’ll show how government largesse might even give a defaulter free housing under the proposed plan. This stuff gets nuttier by the day …

* * * * *

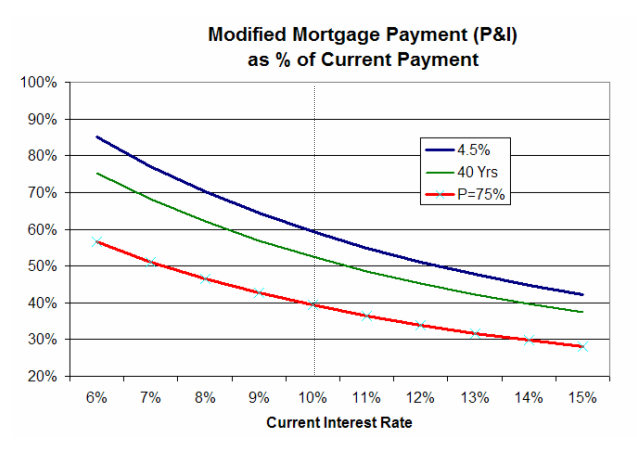

Technical Stuff

Below is a graphical display of the above math. The top line is reducing the interest rate to 4.5%; the middle line reduces the interest rate to 4.5% and extends the term to 40 years; the bottom line reduces the interest rate to 4.5%, extends the term to 40 years, and writes off 25% of the loan balance.

The takeaway: within a representative range of original interest rates, modified mortgage payments can be roughly halved by simply cutting the interest rate to 4.5% and extending the loan term to 40 years.

* * * * *

Want more from the Homa Files?

Click link => The Homa Files Blog