Earlier this week, President Obama turned on a rhetorical dime and rebranded “healthcare reform” as “insurance reform”. Attacking insurance companies as profiteers and the root cause of spiraling healthcare costs.

Many naive Americans, will likely buy-in to the pitch . After all, it’s easy to hate insurance companies since they force us to give up our current doctors in favor of less costly ones, deny us the “right” to have certain procedures done, make us co-pay for drugs and services, and raise our premiums to cover the bloated medical expenses of obese smokers. Those guys are downright evil, right ?

The argument is standard liberal dribble. As typical, it falls apart when subjected to factual analysis.

Below is an analysis that I posted last fall.

Bottom line: (1) health insurance companies don’t make all that much money, and (2) if you think that insurance companies deny a lot of procedures and claims, just wait until government rationing of healthcare kicks in.

* * * * *

Originally posted 09-09-08

http://homafiles.info/2008/09/09/health-insurance-those-health-insurance-companies/

* * * * *

In the book Crunch, liberal economist Jared Bernstein criticizes health insurance companies, asserts that:

- “Other countries with advanced economies save a lot by taking the insurers out of the picture. They employ either single-payer or heavily regulated systems, in which either the government is the exclusive insurer or private insurers must provide specified, the subsidized coverage to all … costs are held down by taking advantage of the huge risk pool — the healthy majority subsidizes the sick minority … and, insurer’s profits are weeded out of the system.”

- “Private insurers have an incentive to prevent people from getting all the care they think they need. Insurers are in the for-profit sector, so they spend time and resources trying to avoid making payouts. “

These are oft repeated refrains from folks who advocate government administered universal heath insurance.

* * * * *

I think this argument displays a remarkably shallow understanding of what health insurance companies do, how much money they make, and how they make it. And. it places a remarkably high level of confidence in government administered programs (think, the FDA chasing down salmonella sources).

* * * * *

First, what is the financial upside if all health insurance companies’ profits are eliminated and put in the national bank as economic cost savings.

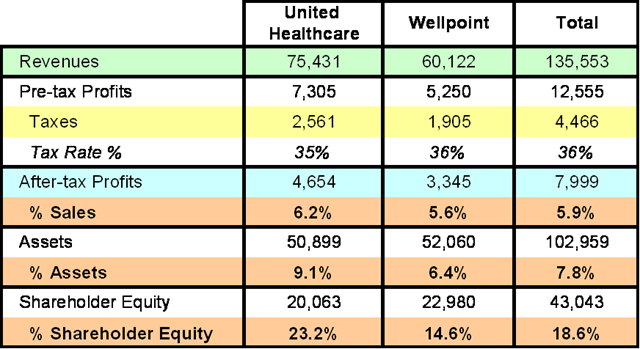

Well, for openers, the health insurance companies — don’t make all that much money. Consider the 2007 financial results for the two biggest “pure” health insurance companies: United Health Care and Wellpoint.

Note that pre-tax profits are about 9% of revenues [12,555 divided by135,553]. About 1/3 of the pre-tax already goes to the government in taxes; about 2/3’s (6% of revenues) drops through to the bottom line.

Currently, U.S. health care expenditures are about $2,1 trillion (just over $7,000 per person). Of that, roughly half is “sourced” from the government via Medicare and Medicaid. Of the half that is private pay, about 2/3’s ($725 billion ) goes through health insurance companies — the other 1/3 is out of patient’s pockets or “other” (e.g. charitable gifts to medical centers).

So, what’s the financial upside if all health care insurers were “disintermediated” and their profits were banked as economic cost savings to the system ?

Well, assuming that the rest of the healthcare insurance companies have profitability profiles comparable to United and Wellpoint — there’s a pre-tax profit of 9% that applies to $725 billion in revenues — or roughly $65 billion dollars.

But wait, the government is already getting about 1/3 of that in taxes.

So, the net gain is at most $40 to $45 billion, or about 2% of the $2.1 trillion in total healthcare spending. Why “at most” ?

Simple, because it assumes that the government will be able to administer the programs as efficiently as the private companies. Call me cynical, but I doubt it.

* * * * *

On the second point, that health insurance companies reject claims and refuse to authorize treatment as a means of boosting their.bottom lines.

Well, that’s at most partially true, and catches the government administration folks in a circular argument.

First, about 1/3 of health insurance companies’ transactions volume is administrative processing done in support of companies (usually big ones) that choose to self-insure. That is, the self-insuring companies take all of the risk, and only pay the insurance companies a fee (that includes profit, of course) for negotiating with health care suppliers and processing transactions — in conformance with terms, conditions, and rules dictated by the companies. There are agreed to standards that are enforced.

The other 2/3’s of their transaction volume is strictly premium based. If more treatments are authorized, costs go up and premiums go up to cover them. If treatments are denied, costs go down, and the competitive market pushes premiums down,It’s that simple.

* * * * *

Want more from the Homa Files?

Click link => The Homa Files Blog

* * * * *

July 22, 2009 at 12:37 pm |

Ken-

Good analysis, but the numbers are a little dense. I graphed them to make the message stand out to the layman.

http://www.consultantninja.com/2009/07/us-health-care-costs.html

July 24, 2009 at 4:11 am |

Thanks for sharing the information on health insurance company. The date you have provided is very helpful for creating a project on it.