In a prior post, we walked through the impact if Obama selectively lets the parts of the Bush tax cuts expire in 2011 — those parts that effect individuals earning more than $200,000 and couples earning more than $250,000.

In a nutshell, here’s what we concluded …

- The tax rate on capital gains will go up 5% … and the tax rate on dividends will go up at least 5% (to the capital gains tax rate) and maybe all the way up to ordinary income tax rates.

- For ordinary income, the effective (not marginal) tax rate increase on ordinary income will be about 1/2% for each $100,000 of taxable income (i.e. ordinary income plus dividends and capital gains) over $200,000.

For example, assume a couple has $200,000 in taxable ordinary income and $100,000 in dividends and capital gains, giving them total taxable income of $300,000. Their tax hit will be about $6,000 — $5,000 from the increase in dividend and capital gains tax rates (5% X $100,000) and $1,000 from the increase in the effective rate on ordinary income ($300,000 minus $200,000 = $100,000 => 1/2% rate increase times $200,000 = $1,000). In rough numbers, their income taxes would go from $67,000 to $73,000 — an increase of almost 9% — and their effective tax rate would go from 21% to over 24%.

But, that’s only part of the story.

Remember that the original Senate bill funded roughly 1/2 of ObamaCare from MediCare cuts and roughly 1/2 from an excise tax on employer provided Cadillac health insurance plans — a plan originally teed up by Obama. When the unions marched on the White House and reminded the President who got him elected, Obama recalibrated upward the threshold defining a Cadillac plan, delayed the implementation of that tax until 2018, and replaced the lost tax revenue with a supplemental 3.8% payroll tax on AGI (Adjusted Gross Income — which includes ordinary income plus dividends and capital gains) over $200,000 — starting in 2013

Technical note: The base Medicare tax rate is currently applied as a payroll tax on so-called earned income. Employees pay 1.45% and employers are required to match the 1.45% — for a total of 2.9%. Under ObamaCare, for “unearned income” — mostly dividends and capital gains — there is no employer per se, so the taxpayer is charged the full 2.9% base … plus, a supplemental .9% was added on for good measure — raising the total to 3.8%

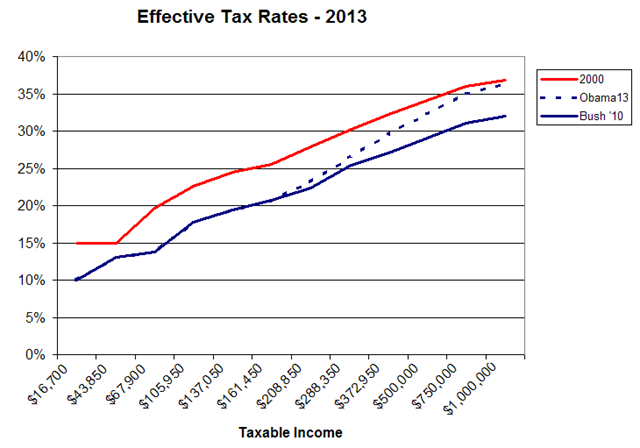

So, comparing 2013 to the current tax rates

- The tax rate on capital gains will go up 5% … and the tax rate on dividends will go up at least 5% (to the capital gains tax rate) and maybe all the way up to ordinary income tax rates.

- For ordinary income, the effective (not marginal) tax rate increase on ordinary income will be about 1/2% for each $100,000 of taxable income (i.e. ordinary income plus dividends and capital gains) over $200,000.

- There is a 3.8% “payroll tax” on all AGI over $200,000 — that includes ordinary income plus dividends and capital gains.

Let’s rework our example …

Again, assume a couple has $200,000 in taxable ordinary income and $100,000 in dividends and capital gains, giving them total taxable income of $300,000.

Their tax hit (versus 2009) will be about $9,800 …

- $5,000 from the increase in dividend and capital gains tax rates (5% X $100,000)

- $1,000 from the increase in the effective rate on ordinary income ($300,000 minus $200,000 = $100,000 => 1/2% rate increase times $200,000 = $1,000).

- $3,800 in additional “payroll taxes” ($300,000 minus $200,000 = $100,000 times 3.8% = $3,800

In rough numbers, their income taxes would go from $67,000 to $76,800 — an increase of almost 15% — and their effective tax rate would go from 21% to over 25.5%.

Keep in mind, that this is just Federal income taxes. Add on another 5% to 10% for state and local income taxes … then draw your own conclusions re: fairness and effect on the economy. …

* * * * *

Here’s a handy tool for estimating effective tax rates now, and prospectively in 2013.

* * * * *

Next up: The triumphant return of the marriage penalty