As oil prices go up, financial speculators are garnering a lot of press and political attention, potentially obscuring the importance of commodities hedging to commercial operations (i.e. companies that actually use the oil).

When there is a scarcity projected for critical commodities — the key “factor inputs” to a company’s operations (e.g. oil for airlines) — or when prices on critical commodities are expected to increase — many companies will “forward buy” the commodities — i.e., hedge them .

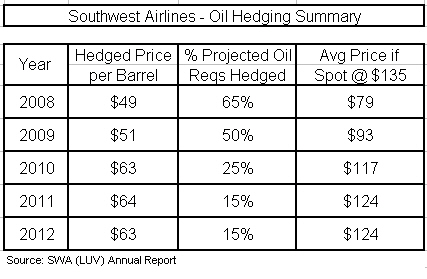

One of the ways that Southest Airlines keeps costs (and prices) comparatively low has been by hedging oil. For example, SWA bought 65% of its projected 2008 fuel requirements (roughly 1.5 billion gallons, 35 million barrels) in advance — at an average price of $49 per barrel.

A couple of observations:

- Only well capitalized companies can substantially hedge key commodities — that rules out most airlines.

- Financial speculators certainly push up the price of futures contracts — though the “players” may eventually be left hanging if spot prices fall.

- Even SWA will feel the pressure of the ‘hot’ futures markets starting in 2010 — when their proportion of relatively cheap hedged oil falls below 50%.

Heads-up to politicians: If an operating company such as SWA hedges via exchange-traded futures contracts, then raising the margin requirements on future contracts would require an enormous inflow of capital. For example: SWA uses about 35 million barrels of oil annually. At $135 per barrel, that’s almost $5 billion per year. So, if SWA hedges 50% of their oil requirement over a 4 year time horizon (as they averaged for the past couple of years), then SWA would need another $10 billion in capital to support the higher margin requirements. As a frame of reference, SWA currently has $18 billion in “total assets” (e.g.planes. airport facilities). That would be a challenge for them, and an impossibility for more financially fragile airlines. (Note: I’m not sure if SWA hedges via exchanged-traded futures contracts — they may contract directly with oil suppliers — and be outboarded from exchange margin requirements)

July 24, 2008 at 11:19 pm |

[…] in 15 months, and a shrinking percentage of its fuel needs are covered over the next four years. Check out this table – by 2012 the company will have just 15% of its fuel needs under hedging contracts, and if oil […]