TakeAway: Big test markets are very old school. Today, test marketing is done through “alternative venues”.

* * * * *

Innosight, STRATEGY & INNOVATION, Thinking Outside the (Big) Box, September 16, 2009

Market experimentation in CPG often requires thinking “outside the (big) box (store)”.

The results of tests run in alternative channels can offer evidence to support (or refute) launch in the traditional and concept refinement in advance of such a launch.

Further, in many cases these channels can represent not only a venue for experimentation but also an early or alternate form of distribution.

The bottom line? Don’t focus on volume when running experiments.

Rather, focus intently on speed, affordability, connecting directly with consumers, and concept refinement.

* * * * *

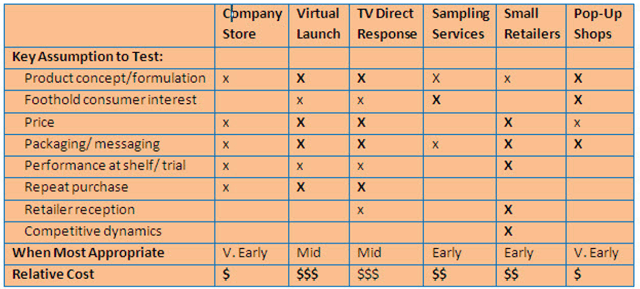

6 out-of-the-box alternatives: the company store, a virtual launch, TV direct response, product sampling services, small retailers and temporary pop shops.

1. Give It a Spot in the Company Store

Offering a new product internally can enable a good-enough approach across several dimensions (i.e., packaging, messaging). The price tag is cheap, and the testing can happen very quickly. Overall, to get an early read on consumer appetite for a new idea, the company store offers a lot of advantages.

2. Leverage Cyberspace with a Virtual Launch

Want to bypass the retail channel altogether when testing a concept? The Internet enables manufacturers to conduct small-scale launches that do just that by setting up simple websites with order-taking and fulfillment capabilities.

Virtual launches offer a lot of other advantages when testing assumptions around new concepts.

First, such launches enable rapid testing of consumer response to formulation, packaging, and branding

without the crippling cost of a full-scale launch.

Second, such launches can create buzz as they can attract early adopters, bloggers, Twitter and Facebook users, and even the increasing numbers of

mainstream press who are listening to these channels.

Third, manufacturers are able to gather valuable consumer information not possible through traditional channels, including feedback (i.e., comment

boxes, chat boards), purchase behaviors (i.e., trial vs. repeat), and customer characteristics (i.e., location, demographics).

P&G has been very active in its experimentation with virtual launches with products including Crest Whitestrips, Pampers Change ‘N Go, Swash by Tide, and Align GI.

In the case of Crest Whitestrips, a virtual launch on whitestrips.com and in select dental offices generated unexpectedly high sales ($23 million from August 2000 to May 2001) and led to an acceleration of the retail launch timeline.

3. Reach for the TV Waves with Direct Response

Along the same lines as the virtual launch, television can offer a unique placement opportunity for manufacturers seeking input on product, pricing, trial/repeat, marketing, messaging, and a host of other product dimensions.

These channels are typically most applicable for more complex or new-to-market products benefiting from such a high-touch sales model.

The two most common alternatives are home shopping networks (i.e., QVC) and infomercials.

Home shopping networks offer a captive audience, live product demonstration, and rich data analytics. This combination enables rapid iteration of messaging based on near real-time sales data.

QVC, for example, boasts an 80+ million household audience to its 24/7 storefront.

Infomercials offer similar advantages to home shopping networks, with a twist.

First, longer formats make them even more applicable for complicated sales models (i.e., devices, new platforms of products, new categories).

Second, higher investment costs in the form of production make them more appropriate for later-stage tests versus a home shopping placement.

Infomercials have also served as stepping stones for many products that have gone on to reach broader audiences. Looking for examples? Think of products like OxiClean (now distributed broadly in FDM channels, and Proactiv available online and through kiosks.

4. Consider Sampling Services

Sampling services often cater to early adopters seeking the newest products on the market. While these solutions do not offer insight on pricing or at-the-shelf behavior, they do offer manufacturers the opportunity to glean valuable early perspectives on certain dimensions (i.e., formulation, packaging, marketing) before a product is ready for the mass market.

Other advantages of such services include being quick to launch, having built-in consumer bases, and incorporating a feedback protocol.

5. Remember that Good Things Come in Small Boxes

Sometimes a more traditional shelf setting is required. In these types of situations, small independent retail outlets can provide a great alternative for under

the radar testing of new products.

For personal care products, spas and salons can provide very relevant data points.

For food products, self-serve restaurants, gourmet stores, or health food stores are a good bet.

For beverages, bodegas or self-serve restaurants get the job done.

All of these settings can provide consumer insights similar to the traditional channel shelf in a smaller scale experiment, often with the added advantage of providing feedback from the proprietor or salesperson.

6.Get Focus Fast with a Pop-Up Shop

Have a defined sense of your foothold consumer but unsure if the concept will resonate?

Setting up a “pop-up shop” in close proximity of your target audience can quickly provide valuable insights at a low price tag.

Think broadly and you’ll surely find that appropriate venues can be found for almost all consumer segments.

Interested in college kids? Try a university campus or bookstore.

Aiming at athletes? Outside a gym might be a good bet.

Have your sights on parents of young kids? A community fair will surely provide a captive audience.

Urban youth? Hit the local basketball courts.

Another twist on the physical pop-shop is to leverage a vending kiosk or a mobile truck offering.

A recent, interesting example of this type of approach is the Coke Freestyle beverage dispenser. Through this novel vending machine, Coke is able to offer over 100 different varieties of beverages (i.e., soda, tea, juice and water) by combining different “micro-doses” from about 30 cartridges in the machine.

Yes, the concept offers mass customization and drives much greater choice for the consumer. Beyond that, however, the machine offers Coke the opportunity to experiment with different flavors and beverages and to get instant feedback on consumer uptake by geography through RFID technology

present on the cartridge.

This type of vending experiment offers enormous cost savings versus the traditional approach of testing a concept by bottling and pushing through the traditional distribution channel to separate winners from losers.

* * * * *

Full article:

http://www.innosight.com/innovation_resources/article.html?id=843

* * * * *

SHARE THIS POST WITH FRIENDS & FAMILY

Like this:

Like Loading...