Bottom line: I wondered why pharma companies got in the ObamaCare canoe and promised cutting prices by $8 billion.

The answer should have been obvious: all for show.

They’re hustling to inflate prices to establish a much higher base from which they can back out the “cuts”.

In other words, the post-reform prices will be right where they had planned them before the faux show of ObamaCare support.

Imagine that … Team Obama getting snookered,

* * * * *

Excerpted from NY Times: Drug Makers Raise Prices in Face of Health Care Reform, November 15, 2009

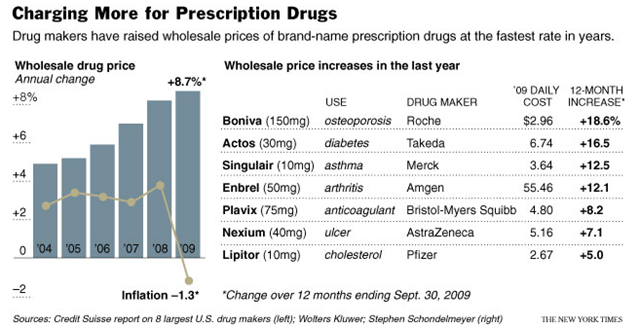

Even as drug makers promise to support Washington’s health care overhaul by shaving $8 billion a year off the nation’s drug costs after the legislation takes effect, the industry has been raising its prices at the fastest rate in years.

The industry stands to gain about 30 million customers with drug insurance from the legislation pending in Congress. But the industry also faces the prospect of tougher negotiations from both public and private buyers as the government tries to squeeze savings out of the health system.

In the last year, the industry has raised the wholesale prices of brand-name prescription drugs by about 9 percent, according to industry analysts. That will add more than $10 billion to the nation’s drug bill, which is on track to exceed $300 billion this year. By at least one analysis, it is the highest annual rate of inflation for drug prices since 1992.

Drug makers say they have valid business reasons for the price increases. Critics say the industry is trying to establish a higher price base before Congress passes legislation that tries to curb drug spending in coming years.

There was a similar pattern of unusual price increases after Congress added drug benefits to Medicare a few years ago, giving tens of millions of older Americans federally subsidized drug insurance. Just as the program was taking effect in 2006, the drug industry raised prices by the widest margin in a half-dozen years.

The drug companies say they are having to raise prices to maintain the profits necessary to invest in research and development of new drugs as the patents on many of their most popular drugs are set to expire over the next few years.

The drug industry has actively opposed some of the cost-cutting provisions in the House legislation, which passed Nov. 7 and aims to cut drug spending by about $14 billion a year over a decade.

But the drug makers have been proudly citing the agreement they reached with the White House and the Senate Finance Committee chairman to trim $8 billion a year — $80 billion over 10 years — from the nation’s drug bill by giving rebates to older Americans and the government.

But this year’s price increases would effectively cancel out the savings from at least the first year of the Senate Finance agreement. And some critics say the surge in drug prices could change the dynamics of the entire 10-year deal.

http://www.nytimes.com/imagepages/2009/11/16/business/16drugprices_graphic.html

Full article:

http://www.nytimes.com/2009/11/16/business/16drugprices.html