From IBD, 15 reasons why a government takeover of the finest medical system in the world makes no sense at all:

1. The people don’t want it!

This should have some bearing on decision-making. In the latest Rasmussen poll, 53% opposed Obama’s reform while 42% were in favor. More than four in 10 “strongly” opposed; just two in 10 “strongly” favored. This jibes with other surveys.

2. Doctors don’t want it!

A survey of 1,376 practicing physicians found that 45% of all doctors would consider leaving their practices or taking early retirements if the proposed reforms became law … nearly 30% said they’d quit the profession under the plans being considered.

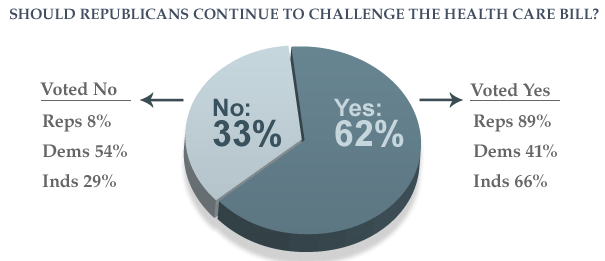

3. Half the Congress doesn’t want it!

Not a single Republican backed the health care bill that cleared the Senate on Christmas Eve 60-39. The lone Republican “aye” in the House has since switched to “no.” Adjusting for reps who are no longer in Congress, the House vote today at 216-215 in favor.

Note: Members of Congress have already exempted themselves from whatever they inflict on us.

4. People are happy with the health care they’ve got!

Polls show that 84% of Americans have health insurance and satisfaction rates average 87%.

5. It doesn’t even cover all the people they set out to cover!

Supporters of government-run health care say there are as many as 47 million Americans — 9 million to 10 million of them illegal aliens — without medical insurance. The plans, however, will put only 31 million of the uninsured under coverage.

6. Costs will go up, not down!

Democrats say their plans will cost less than $1 trillion over the first decade, but independent analysts put the cost at $2.5 trillion over the first 10 years.

7. Real cost controls are nowhere to be found!

The Democrats are offering no meaningful tort reform that will help push down the high malpractice insurance premiums that are a burden to doctors and their patients. Nor are they considering any other cost-saving provisions, such as allowing the sale of individual health plans across state lines or easing health insurance mandates.

8. Insurance premiums will rise, not fall!

One goal of nationalizing health care is to lower costs, to bend the spending curve downward. Yet, as Democratic Sen. Dick Durbin acknowledged Wednesday, that won’t be the case.

“Anyone who would stand before you and say, ‘Well, if you pass health care reform, next year’s health care premiums are going down,’ I don’t think is telling the truth,I think it is likely they would go up.”

9. Medicare is already bankrupting us!

The Medicare trust fund, which has unfunded obligations of $37.8 trillion, will be insolvent in 2017.

10. There aren’t enough doctors now!

Last month, 26% of physicians said they had been forced to close, or were considering closing, their solo practices. Providing coverage for an additional 31 million Americans when the number of doctors is shrinking won’t improve our health care.

11. The doctor-patient relationship will be wrecked!

The latest IBD/TIPP Poll, taken just last week, found that Americans, by a wide 48% to 26% margin, believe the doctor-patient relationship will decline if the Democrats’ plan is passed.

12. Medical care will also deteriorate!

IBD/TIPP has also found that 51% of Americans believe care would get worse under government control. … 72% disagreed with administration claims that the government could cover 47 million more people with better-quality care at lower cost.

13. Rationing of care is inevitable!

Health care is not an unlimited resource and must be rationed, either by the individual, providers or government. In Britain and Canada, where the government does the rationing, medical treatment waiting lists are sometimes deadly and quite often excessively long.

14. Private health insurers will be destroyed!

Added mandates and price controls will force many insurers to simply get out of the health plan business because it will no longer be profitable.

15. It’s probably unconstitutional!

One way to help bring down the number of uninsured is to demand that those without coverage buy health plans. Constitutional scholars say any such mandate would likely draw a legal challenge.

Sourced from IBD: Why Health Bill Makes No Sense, 03/12/2010

http://www.investors.com/NewsAndAnalysis/Article.aspx?id=527217

SHARE THIS POST WITH FRIENDS & FAMILY