Excerpted from Newsweek: “Getting Real About Health Care

It’s not about coverage. It’s about costs.”, Robert J. Samuelson

Sep 6, 2008

* * * * *

Note: There are roughly 45 million uninsudred people in the U.S. Approximately 1/3 are not legal citizens; approximately 1/3 are in the top 1/2 of wage earners (i.e. over the $50,000 median); approximately 40% are 19 to 34, relatively healthy and, in effect, choose to self-insure.

* * * * *

Summary; Emphasis should be on fundamental restructuring of costs: more electronic record-keeping, better case management, fewer dubious tests and procedures (i.e. unnecessary, duplicative), contained end-of-life treatment.

* * * * *

Article

46 million Americans … or almost one in seven lack health insurance.

By impressive majorities, Americans regard this as a moral stain. Sen. Ted Kennedy echoed the view of many that health care is a “right” that demands universal insurance. This is a completely understandable view and one that is, I think, utterly wrong.

* * * * *

Health care should be at the top of the agenda. But the central problem is not improving coverage. It’s controlling costs.

In 1960, health care accounted for $1 of every $20 spent in the U.S. economy; now that’s $1 of every $6, and … it could be $1 of every $4 by 2025. Ponder that: a quarter of the U.S. economy devoted to health care.

Countless studies have shown that many diagnostic tests, surgeries and medical devices are either ineffective or unneeded.

Greater health spending should not have the first moral claim on our wealth, because its relentless expansion is slowly crowding out other national needs.

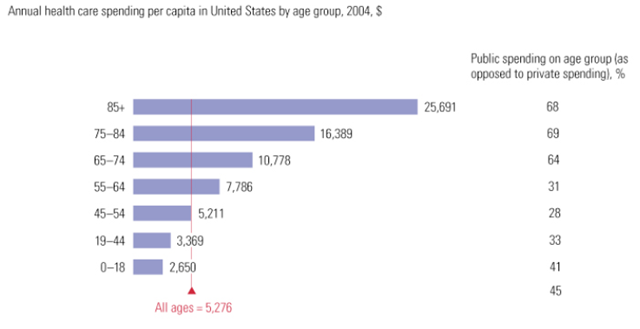

For government, higher health costs threaten other programs—schools, roads, defense, scientific research—and put upward pressure on taxes. For workers, increasingly expensive insurance depresses take-home pay, as employers funnel more compensation dollars into coverage. There’s also a massive and undesirable income transfer from the young to the old, accomplished through taxes and the cross-subsidies of private insurance, because the old are the biggest users of medical care.

* * * * *

It is widely assumed that health care, like most aspects of American life, shamefully shortchanges the poor. This is less true than it seems.

Data show that, on average, annual health spending per person—from all private and government sources—is equal for the poorest and the richest Americans. In 2003, it was $4,477 for the poorest fifth and $4,451 for the richest.

The reason: government already insures more than a quarter of the population, including many of the poor. Medicare covers the elderly; Medicaid, many of the poor and their children; SCHIP (State Children’s Health Insurance Program), more children.

Another reason, stems from the skewing of health spending toward the very sick and dying; 10 percent of patients account for two thirds of spending. People in this unfortunate group, regardless of income, get thrust onto a conveyor belt of costly care: long hospital stays, many tests, therapies and surgeries.

* * * * *

That includes the uninsured. In 2008, their care will cost about $86 billion, … The uninsured pay about $30 billion themselves; the rest is uncompensated.

Of course, no sane person wants to be without health insurance, and the uninsured receive less care and, by some studies, suffer abnormally high death rates. But other studies suggest only minor disadvantages for the uninsured.

* * * * *

We need more realism on health care. The trouble with casting medical-care as a “right” is that this ignores how open-ended the “right” should be and how fulfilling it might compromise other “rights” and needs.

What makes people healthy or unhealthy are personal habits, good or bad (diet, exercise, alcohol and drug use); genetic makeup, lucky or unlucky, and age. Health care, no matter how lavishly provided, can only partially compensate for these individual differences.

* * * * *

There is a basic moral and political dilemma that most Americans refuse to acknowledge. What we all want for ourselves and our families—access to unlimited care paid for by someone else—may be ruinous for us as a society.

Sensible limits must somehow be imposed.

* * * * *

The crying need now is not to insure all the uninsured. This would be expensive (an additional $123 billion a year, estimates the Kaiser study) and would provide modest health gains at best since 40% of the uninsured are young (19 to 34) and relatively healthy.

The compelling need now is to limit the runaway increases in spending that make private and government insurance more expensive and may not deliver significant health improvements.

* * * * *

Both McCain and Obama have health-care proposals that … largely ignore the massive health-care challenge already sitting in the government’s lap: Medicare.

By some studies, 30 percent of Medicare spending may go to unneeded services that do not enhance recipients’ well-being.

Medicare is so large and influential that by altering how it operates, government can reshape the entire health-care system. This would require changes in rules and reimbursements to encourage more electronic record-keeping, better case management, fewer dubious tests and procedures, and a fairer sharing of costs between the young and the old.

The work would be unglamorous and probably unpopular. But if the next president won’t—or can’t—do it, his presidency will fail in one fateful way.

* * * * *

Full article:

http://www.newsweek.com/id/157573

* * * * *

Want more from the Homa Files?

Click link => The Homa Files Blog

SHARE THIS POST WITH FRIENDS & FAMILY