Excerpted from Tax Foundation: “Both Candidates’ Tax Plans Will Reduce Millions of Taxpayers’ Liability to Zero (or Less) “, Scott Hodge, September 19, 2008

* * * * *

Ken’s Notes:

1. The statistics below consider only tax filers. Approximately 20% of adults don’t file returns — presumably since their incomes are zero or below the filing limits.

2. The impact of the McCain proposal surprised me. From a tax structure perspective, the plans are a push. Of course, Obama would layer the health insurance provisions as added spending (versus reduced revenue).

3. Isn’t anybody concerned that a minority of citizens will be carrying the entirety of the tax burden ?

* * * * *

Article Summary

Over the past two decades, lawmakers have increasingly turned to the tax system rather than direct spending programs to funnel money to targeted groups of Americans, furthering some social or political goal. As a result, millions of Americans have been effectively removed from the income tax payment system while the tax code has been made more complicated to comply with and more difficult to administer. The tax plans of both the presidential candidates would exacerbate this situation greatly.

* * * * *

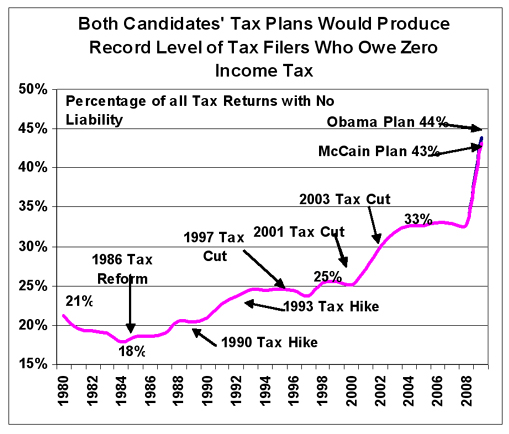

1.3 of filers currently pay no income tax

One of the biggest challenges facing both John McCain and Barack Obama in their commitment to provide tax relief to working-class Americans is the simple fact that millions of them already pay no personal income taxes.

According to the most recent IRS statistics for 2006, some 45.6 million tax filers—one-third of all filers—have no tax liability after taking their credits and deductions. For good or ill, this is a dramatic 57 percent increase since 2000 in the number of Americans who pay no personal income taxes.

* * * * *

Obama or McCain — Essentially a Push (much to my surprise)

Tax Foundation estimates show that if all of the Obama tax provisions were enacted in 2009, the number of these “nonpayers” would rise by about 16 million, to 63 million overall. If all of the McCain tax proposals were enacted in 2009, the number of nonpayers would rise by about 15 million, to a total of 62 million overall.

* * * * *

Big Issue: Refundable Tax Credits = Negative Income Taxes

The tax code has always contained provisions that reduce the income tax burden for low-income workers, such as the standard deduction, personal exemption, and dependent exemption.

Between 1950 and 1990, the percentage of tax filers whose entire tax liability was wiped out by these provisions averaged 21 percent. Since then, lawmakers have expanded credits—such as the earned income tax credit (EITC)—while creating a plethora of new credits, including the child tax credit, the HOPE credit, lifetime learning credit, and the credit for adoption expenses.

Most tax credits can only reduce a taxpayer’s amount due to zero, but the EITC and the child tax credit were also made refundable, meaning that taxpayers are eligible to receive a check even if they have paid no income tax during the year. Those tax returns have become, in effect, a claim form for a subsidy delivered through the tax system rather than a direct payment from a traditional government program like welfare or farm supports.

* * * * *

As shown in Table 1 below, the Tax Foundation estimates that there will be 47 million tax returns with zero income tax liability in 2009 under current law. That’s one-third of all tax returns, and those 47 million tax returns represent 96 million individuals.

Both the McCain and Obama plans would increase this number by expanding existing tax benefits or creating new ones.

* * * * *

Senator McCain is proposing one expanded provision—the dependent exemption—and one new credit, a $5,000 refundable health care tax credit.

Taken together, the McCain proposals would increase the number of nonpayers by about 15 million, bringing the total number of taxpayers who pay no personal income taxes to 62 million, roughly 43 percent of all tax filers. Almost all of this is due to McCain’s health care credit, which dramatically realigns health care incentives and gives people a powerful motive to buy health insurance. This tax provision has a bigger impact on cutting people’s taxes than any single proposal from either party.

* * * * *

Obama uses a longer list of smaller tax credit ideas to reduce a similar number of taxpayers’ liability to zero. The Obama plan contains seven new provisions, including a new “Making Work Pay Credit,” a “Universal Mortgage Credit,” and a plan to eliminate income taxes for seniors earning under $50,000. About 16 million people who are currently paying at least a little income tax would see their liability zeroed out, bringing the total to 63 million, or 44 percent of all tax returns.

* * * * *

Major structural tax changes enacted during the 1980s contributed greatly to the doubling of nonpayers. Perhaps the most significant was indexing the tax brackets in 1985 to prevent inflation from pushing people into higher tax brackets. Also, the Tax Reform Act of 1986 nearly doubled the personal exemption and replaced the zero-bracket with the basic standard deduction for nonitemizers.

Since the early 1990s, however, lawmakers have increasingly used the tax code instead of government spending programs to funnel money to groups of people they want to reward. Credits have been enacted to subsidize families with children, college students, and purchasers of hybrid cars, just to name a few of the most well known. In terms of tax revenue, the most significant of these socially targeted credits was the $500 per-child tax credit enacted in 1997. The 2001 and 2003 tax bills doubled the value of the credit to $1,000 and added a refundable component.

* * * * *

Quite aside from the fact that these refundable credits remove millions from the roster of Americans who support the government by paying the income tax, these credits have some undesirable effects.

Added complexity. The explosion of tax credits has added a tremendous amount of complexity to the tax code, especially for low-income Americans who are the supposed beneficiaries of the programs. The EITC is so complicated that more than three-quarters of those claiming it pay a tax preparer to complete their forms.

Hidden marginal tax rate increases. To withhold the benefit of these credits from “rich people,” the definition of which changes from law to law, each of these credits has a phase-out range—that is, a range of income where the taxpayer has to pay back the credit that he no longer qualifies for. As a result, taxpayers in the phase-out range face unexpectedly high effective marginal tax rates.

Narrowing the tax base. Expanding existing credits or adding new ones pushes people who used to pay taxes into the nonpayer range, shrinking the tax base and requiring higher taxes on everyone else. Undesirable volatility in federal revenue is the likely result, as the incomes of higher-income taxpayers include more business, dividend, and capital gains income which fluctuate much more wildly than wages.

* * * * *

Full article:

http://www.taxfoundation.org/publications/show/23631.html

* * * * *

Want more from the Homa Files?

Click link => The Homa Files Blog

SHARE THIS POST WITH FRIENDS & FAMILY

![[Chart]](https://i0.wp.com/s.wsj.net/public/resources/images/NA-AS811_HOMEHE_NS_20080928193227.gif)

![[Chart]](https://i0.wp.com/s.wsj.net/public/resources/images/NA-AS653_RETIRE_NS_20080921192028.gif)